Introduction

In today's farming environment of extreme price volatility and large debt commitments, most livestock producers need the security of one or more of the advantages offered by price risk management. Livestock producers who are selling products or purchasing inputs can do one of two things when making pricing decisions: accept the market price when they are ready to deliver products or purchase inputs, or reduce input and product price risks by using price risk management tools. One of these price risk management opportunities is available through futures markets contracts. This publication explains how livestock producers can use futures markets to manage price risk.

Who Uses the Futures Market?

Two groups are interested in futures trading -- speculators and hedgers. Speculators enter the futures market with the objective to make a profit from changes in futures prices. They establish a price for a commodity that they neither currently own nor have committed to produce. They have no intention of either delivering or accepting delivery of the product traded. Speculators trade to make a profit from price level changes. They may not even know what a soybean looks like, or the difference between a Holstein and a Hereford. However, they do know (or think they know) that the price of beans or cattle is too low (or high) and hope that by buying (or selling) futures contracts today they can later liquidate the contracts at a profit. So the key to speculating is buying low and selling high or selling high and buying low. Sounds easy, doesn't it? Well, before you jump in, be assured that the majority of futures market speculators (in fact, almost 90 percent) lose money at some point.

The other trader in the market is the hedger. The hedger establishes a price for a commodity that is either currently owned or committed for production and that will be delivered at some time in the future (e.g., grains, oilseeds or livestock), or that will be purchased in the future (e.g., feed ingredients bought by livestock producers, or crops by elevators, gins, etc.). Hedging is exactly the opposite of speculating in the market. Speculators are in the futures market to capitalize on price changes, while hedgers are in the futures market to mitigate the risk associated with price changes. Hedgers want to protect a price that will make them a profit.

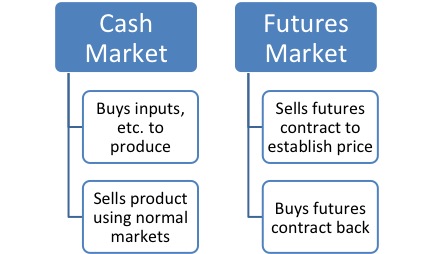

Hedgers as Sellers

Hedgers using the futures market take an offsetting position from the one they have in the cash market. For instance, when hedgers use the futures market to sell, they sell commodity futures contracts to establish a price. They sell because this is the opposite of their buying position in the cash market. Another way to keep this straight is to think of it as pre-selling in the futures market. Then, when the product is actually ready for delivery in the cash market (when they are ready to take the grain to the local elevator, the feeder cattle to auction or their specific cash marketing method), they buy the contracts in the futures market to offset or nullify the previous sale and deliver the product to the local market. Thus, any profits (losses) made in the futures market are to some extent offset by opposite losses (profits) in the cash market. It's similar to a balancing scale -- when one goes up, the other goes down. In terms of money, this places the hedger back at the originally estimated price.

As shown in Figure 1, a hedger who is selling operates in two markets. The action can be shown as follows:

Figure 1. Cash market and futures market flow chart for buying and selling.

Figure 1. Cash market and futures market flow chart for buying and selling.

Speculators, on the other hand, have no product to deliver. If they sell a contract in the futures market, they will have to later buy a contract to offset this previous sale (in the same way the hedger does). But when speculators offset their contracts, they have no product to sell on the cash market to offset losses in the futures market. They profit only to the extent they are able to guess which direction the market is moving. To make a profit, speculators must be able to buy, or offset, at a price lower than the price at which they sold, or they must sell at a price higher than that for which they bought a futures contract.

Hedging is a method of managing price risk by transferring that price risk to speculators. Speculators take on the price risk associated with commodities that they do not own. The reason futures markets exist is to transfer the risk of price changes from those who do not want it (hedgers) to those who want to speculate on these price changes for an opportunity to make a profit.

Most producers who do not use futures markets contracts are speculators in the cash market. They are speculators because they produce or store their products un-priced. They have capital, labor and many other resources committed to the production of the crop or livestock, and they don't know what price they are going to get out of the product until the actual sale day. They are investing money and time into production and actually speculating on whether or not they are going to make a profit or a loss. In this respect, the producer who produces un-hedged is actually in the same position as the speculator in the futures market. The producer is gambling that the selling price will be higher than their cost of production. So, speculators can be found in either the cash market or the futures market.

Contrary to popular belief, speculators serve a very important role in the futures markets by providing liquidity. If it were not for speculators, many futures contracts would fail to trade.

Using the futures market to hedge is a way to trade price risk for basis risk (Basis = Local Cash Price - Futures Price). The reason for trading price risk for basis risk is that prices tend to be more volatile than the basis. The basis can change in time but in general as the futures price increases (decreases) the local price increases (decreases) and the difference is less than that experienced in prices. Interested readers should also consult 禁漫天堂 Extension Bulletin 1406, "Understanding and Using Cattle Basis in Managing Price Risk," to help them better understand the various factors that can affect basis.

So, who are the speculators and who are the hedgers in the market? Speculators may be professional traders (generally short-term traders) who buy and sell contracts and offset them on the same day or after a short period of time. Speculators may also be business people, such as farmers, operating in the futures market in an attempt to make money by anticipating price changes.

Hedgers are producers, processors, handlers, dealers or anyone who uses the markets (either futures or cash markets) to forward price their sales or purchases. Remember, hedging is simply forward pricing. If you use the futures market to forward price, you're a hedger.

Hedgers as Buyers

Some producers may be interested in "locking-in" purchase prices. Examples would be dairy, beef and pork producers purchasing feed ingredients, or elevators, gins or feed manufacturers that will be purchasing grains to re-sell. In any case, buyers can use futures to "pre-buy" the commodities that they will later purchase in the cash market.

When a hedger uses the futures market to buy a commodity input, he buys the appropriate futures market contract to establish a purchase price. He buys because this is the opposite of his selling position in the cash market. Another way to keep this straight is to think of it as pre-buying in the futures market. When it's time to purchase the commodity in the cash market (when you are ready to buy the feed or take delivery of the grain to merchandise), you sell the contracts in the futures market to offset, or nullify, the previous buy and take delivery of the product in your local market.

The term "locking-in" a price actually means locking-in a price range. The price range that is locked in is determined by how much the basis changes from when a hedger starts using the futures market to hedge a commodity.

The net effect is the same as with the selling hedge -- any profits (losses) made in the futures market are to some extent offset by opposite losses (profits) in the cash market. It's similar to a balancing scale -- when one goes up, the other goes down. In terms of money, this places the hedger back at the price he originally positioned himself for.

Perhaps the best way to show this is take a real-world example and show how the two markets offset each other and allow the hedger to price without actual delivery to futures market points.

How Hedging Works

Since a hedger operates in two markets -- the cash market and the futures market -- we can use some numbers to show exactly how this works. Let's assume it is mid-November and you are a feeder cattle producer interested in hedging a part of your cattle that you will market in mid-April.

The first step for the hedger is to choose which contract to use. The CME Feeder Cattle (FC) contract represents 50,000 pounds of feeder cattle weighing 650-849 pounds (see info box). Therefore, the CME FC contract represents 59-77 head of feeder cattle, depending on their weight. See Table 1 for the specifications of the Feeder Cattle Futures Contract.

- The CME Feeder Cattle (FC) contract:

- While the Feeder Cattle (FC) contract is for 50,000 pounds of steers weighing 650-849 pounds each and graded as medium-large frame #1-#2 muscling, cattleman can utilize the FC futures to hedge calves and feeder cattle of all weights and sexes. The key is knowing the basis between what will be sold and the FC contract.

- It is extremely rare for cattle producers to have exactly 50,000 pounds of calves to sell. As a result, the difference in the actual pounds marketed versus the pounds covered with an FC contract(s) will be over or under covered. The number of calves required to fill one FC contract at various delivery weights is shown in Table 2.

- A word of caution: Potential hedgers are encouraged to estimate as closely as they can the number of contracts they will need. More often than not, it is better to have more cattle than contracts. For instance, if you estimate that you will be selling 65,000 pounds of calves, it is better to have only one FC contract, not two.

You will be interested in the futures contract that matures closest to, but not before, the time your cattle are ready to market. Since there is an April futures contract and the cattle will be priced in April, you select the April futures contract. The current futures market price for this futures contract can be viewed by looking either on the Internet or an electronic marketing service. Let's assume the April futures closed today at $175 per hundredweight (cwt.). Now you are faced with two basic questions:

- What does the futures quote of $175/cwt. mean through a hedge?

- Once the hedge price is known, how is the price "locked in"?

Let's break down each of these questions. What does a futures price mean? The $175/cwt. April 20xx Chicago Mercantile contract price represents the weighted average value of 650- to 849-pound medium and large frame #1-2 steers reported by USDA during April 20xx. The local market price will be related to the futures market price during the delivery month, as feeder cattle prices are determined in a national market.

The CME Feeder Cattle futures contract Index is based on the weighted average price of cattle marketed through auctions, direct, video and Internet sales in the 12-state region of Colorado, Iowa, Kansas, Missouri, Montana, Nebraska, New Mexico, North Dakota, Oklahoma, South Dakota, Texas and Wyoming. To be used in the feeder cattle index, cattle must meet the contract specifications. The feeder cattle futures price index is used to settle any open contracts after the termination of trading on the last Thursday of the contract month for that day. Some cattle buyers and sellers also use it to price their cattle.

We can assume local feeder cattle cash prices will move with the futures prices represented by the futures market. Therefore, if feeder cattle futures prices go up, prices at the local market should go up and vice versa. If the hedger knows the historical relationship between the local cash prices and futures market prices (often called basis), he can use the futures market price to determine an estimate of what cattle may sell for in today's local cash markets. This relationship is called basis. Basis is the difference between the local cash price and the futures price (Basis = Local Cash Price - Futures Price). We can rearrange the basis equation to provide an estimate of the local cash price simply by adding the historical basis and today's futures price for the contract month we are interested in (estimated local cash price = historical basis plus today's futures price).

For example, assume that by comparing the historical difference between his local cash market prices in April with April futures prices, the hedger finds an average difference of -$10/cwt. That is, the price of cattle similar to what he plans to sell has averaged $10/cwt. less in the local cash market than the April futures prices on the same day.

Now, the hedger can adjust the futures price to reflect an estimate of delivery in his local cash market. If in April the hedger's local market is $10/cwt. under the April futures price, the future price means $175 + (- $10 basis) results in a local cash price of $165/cwt. This is the local cash price the futures market is currently offering through a hedge for feeder cattle sold in April.

Let's put this in terms of the two markets in which the hedger operates -- the cash market and the futures market -- assuming it is currently November 15.

| Date | Cash Market | Futures Market | Expected Basis |

| Nov 15 | Expected cash price = Futures price + (basis) Expected cash price = $175+(-$10) =$165/cwt. | April FC Futures @ $175/cwt. | -$10/cwt. |

Locking in a Feeder Cattle Price Through a Hedge

Now that the hedger knows what the futures market is offering, how does he go about locking it in if he likes this price? Recall from the previous discussion, the hedger takes an opposite position in the futures market from the one he or she has in the cash market. In this case, the hedger would sell the number of contracts needed to cover the number of feeder cattle to be forward-priced. The hedger is in effect "pre-selling" the cattle in the futures market. Assuming the hedger wishes to price a group of 65 feeders weighing 750 pounds in April, one futures contract will be sold. By calling a broker and placing an order to sell one contract of April Feeder Cattle at $175/cwt., the hedger has an approximate forward price on the 65 head to be sold in April for $165/cwt. ($175 plus the -$10 estimated basis). For this example, the two major costs of hedging -- brokerage commissions and interest on the initial good faith money (margin) -- are ignored.

Now, fast-forward to April. The hedger's cattle are ready to sell either at the local auction market or by some other method. For illustration purposes, we will use the local auction market. The producer takes the cattle to the local market and on the same day buys back the futures contract. The broker notifies the producer that he/she has bought a contract at $180/cwt. while the price on the cattle was $170/cwt. at the stockyards. Now what has happened to the forward-price? Look at the results of the two markets again.

Rising Prices

| Date | Cash Market | Futures Market | Basis |

| November 15 | Expected cash price = Futures price + (basis) or $175-$10 = $165/cwt. | Sell 1 Apr FC Futures @ $175/cwt. | -$10/cwt. (expected) |

| April 15 | Sold 65 head of cattle at local market for $170/cwt. | Bought 1 Apr FC futures @ $180/cwt. | -$10/cwt. (actual) |

| Futures Results: Sold $175 Bought $180 Loss of $5/ cwt. |

Net Price Received = Cash Price + futures gain or loss

Net Price Received = $170 - $5 futures loss = $165/cwt.

The hedge resulted in a net price of $165/cwt., just what the hedger had planned. The gain in the cash market ($180 vs. $175) was just offset by the loss in the futures market, providing the anticipated target price. Of course, had the producer not hedged, he/she would have received a higher price, but if that had been known back in November, why forward-price? In fact, if the hedger knows which way prices are going, why raise cattle? Just speculate in the futures and forget about all the production troubles.

What would have happened if prices had fallen between November 15 and April 15? Look at the action in each market.

Falling Prices

| Date | Cash Market | Futures Market | Basis |

| November 15 | Expected cash price = Futures price + (basis) or $175-$10 = $165/cwt. | Sell 1 Apr FC Futures @ $175.00/cwt. | -$10/cwt. (expected) |

| April 15 | Sold 65 head of cattle at local market for $155/cwt. | Bought 1 Apr FC futures @ $165/cwt. | -$10/cwt. (actual) |

| Futures Results: Sold $175 Bought $165 Profit of $10/cwt. |

Net Price Received = Cash Price + futures gain or loss

Net Price Received = $155 + $10 futures gain = $165/cwt.

Again, the hedger received the $165/cwt. target price even though prices fell from the placement of the hedge until April. Why? Because the loss in the cash market ($155 vs. $165) was offset by a profit in the futures market ($175 vs. $165), giving the hedger a target price of $165/cwt. for the cattle.

Note two things from this example: On November 15, the expected cash price was estimated using the current futures price and the expected basis. Second, the net price received equals the expected cash price. In other words, the hedger locked in exactly the price he wanted, resulting in a perfect hedge. Regardless of which direction prices go, as long as the basis is estimated correctly, the hedge will lock in the target price.

What happens when the actual basis is different from the estimated basis? The following "basis error" example illustrates this situation.

Basis Error

| Date | Cash Market | Futures Market | Basis |

| November 15 | Expected cash price = Futures price - (basis) or $175-$10 = $165/cwt. | Sell 1 Apr FC Futures @ $175/cwt. | -$10/cwt. (expected) |

| April 15 | Sold 65 head of cattle at local market for $153/cwt. | Bought 1 Apr FC futures @ $165/cwt. | -$12/cwt. (actual) |

| Futures Results: Sold $175 Bought $165 Profit of $10/ cwt. |

Net Price Received = Cash Price + futures gain or loss

Net Price Received = $153 + $10 futures gain = $163/cwt.

What has happened? The cash price received in April at the local auction was actually $2/cwt. lower relative to April futures than expected; hence, the net price received is $2/cwt. lower than the expected cash price ($153 vs. $155). Notice, this is the same difference as the estimated -$10/cwt. basis on November 15 and the actual basis of -$12/cwt. on April 15.

The take-home message is that hedging locks in an exact price as long as the estimate of the basis is correct. However, in most practical situations there will be a difference between the actual and estimated basis. The net price and target price will differ by the error in estimating basis.

For our example, we used a cattle producer's hedge. The hedge works the same way for all commodities. To establish a price, you "pre-sell" or sell the number of future contracts to cover the amount of production you wish to hedge. Then when you are actually ready to sell your production, you buy back your futures contracts. You will receive your hedge target price plus or minus the amount you miss on your estimated basis.

Using Futures to Pre-Buy Inputs

In addition to pre-selling, livestock and dairy producers may be interested in pre-buying feed. Stocker operators, feedlots or packers may also be interested in pre-pricing cattle that they will be purchasing later.

Pre-buying using futures contracts has several advantages, including the fact that you do not have to pay for the full amount to be purchased at one time. Rather, by using futures contracts, you can establish a purchase price, subject to the fluctuations of the basis, without tying up your money for a long time. Futures contracts also allow producers to pre-buy inputs without having to store them. This allows producers to use their capital for things other than grain bins or additional cattle-handling facilities.

When hedging an input or something that will be purchased at a later date, the hedging process is similar to what we previously discussed, with the exception of the hedge's initiation. To hedge something that will be purchased later, for instance corn or soybean meal, a hedge is established by "pre-buying" or buying futures contracts. When the input is actually purchased in the cash market, the futures contracts are sold. In this manner, any gain or loss in the futures market prices will be offset by a gain or loss in the inputs' cash market. The actual price paid for the input will miss the original target price of the hedge by the amount the actual basis differs from the estimated basis.

Buying hedges may be initiated (1) in the belief that the commodity will be valued higher later on, (2) in order to make management decisions or (3) in combination with a selling hedge to lock in total profits. No matter what the commodity, the buying hedge is a simple reversal of the futures and cash market actions used for the selling hedge.

A Buying Hedge Example

Suppose it is July 1 and you are a dairy producer who needs 5,000 bushels of corn four months from now. Since there is not a November corn futures contract, you check the December corn futures (remember to select the futures contract month that matures closest to, but not before, you need the corn) and find that the contract is trading at $5.00 per bushel. You must adjust this futures price by your anticipated buying basis come November. If you were going to buy corn from local producers, you might use the basis figures found in "Basis Tables for Georgia Feeder Cattle, Hogs, Corn and Soybeans," since these represent average prices paid to producers byelevators in the different areas vs. futures prices. However, if you were going to buy corn from elevators, you should adjust this basis to account for processing and handling.

Let's suppose you estimate your buying basis in November will be $.50 over the December corn futures price. Now you know what the $5.00 December quote means for corn purchased locally in November (5.00 + .50 basis, or $5.50 per bushel). Let's assume you decide to lock in this price with a hedge. In this case, instead of pre-selling corn you will be pre-buying corn. To price in the futures market, buy the appropriate number of contracts to price in July the corn you will be purchasing on the cash market in November. The following accounts show the actions and results of three different situations using the buying hedge.

Notice that in each situation the net price paid equals the target price as long as the basis has been estimated correctly. When prices rise after the hedge is set, a profit in the futures market is offset by the higher price you have to pay for the corn in the local market. Alternatively, if prices fall after the hedge is set, it means a loss in the futures market, which must be added to the lower price you pay for corn in the cash market. The loss results because you have to sell your futures contract back at a lower price than you bought it.

The basis error section shows, once again, that the target price will equal the net price as long as the basis has been estimated correctly.

Rising Market with a Buying Hedge

| Date | Cash Market | Futures Market | Basis |

| July 1 | Expected cash price = Futures price + (basis) or $5.00 +$0.50 =$5.50/bushel | Buy 1 Dec Corn Futures @ $5.00/bushel | +$0.50/ bushel (expected) |

| Nov 15 | Buy 5,000 bushels of corn locally for $5.75/bushel | Sell 1 Dec Corn Futures @ $5.25/bushel | +$0.50/ bushel (actual) |

| Futures Results: Bought $5.00/bushel Sold $5.25/bushel Profit of $0.25/bushel |

Net Price Paid = Cash Price - futures loss or gain.

Net Price Paid = $5.75 - $0.25 futures profit = $5.50/bushel

Falling Prices with a Buying Hedge

| Date | Cash Market | Futures Market | Basis |

| July 1 | Expected cash price = Futures price + basis or $5.00 +$0.50 =$5.50/ bushel | Buy 1 Dec Corn Futures @ $5.00/bushel | +$0.50/ bushel (expected) |

| Nov 15 | Buy 5,000 bushels of corn locally for $4.75/ bushel | Sell 1 Dec Corn Futures @ $4.25/bushel | +$0.50/ bushel (actual) |

| Futures Results: Bought $5.00/bushel Sold $4.25/bushel Loss of $0.75/bushel |

Net Price Paid = Cash Price - futures loss or gain

Net Price Paid = $4.75 - (- $0.75 futures loss) = $5.50/bushel

Basis Error with a Buying Hedge

| Date | Cash Market | Futures Market | Basis |

| July 1 | Expected cash price = Futures price + basis or $5.00 +$0.50 =$5.50/bushel | Buy 1 Dec Corn Futures @ $5.00/bushel | +$0.50/ bushel (expected) |

| Nov 15 | Buy 5,000 bushels of corn locally for $4.50/bushel | Sell 1 Dec Corn Futures @ $3.75/bushel | +$0.75/ bushel (actual) |

| Futures Results: Bought $5.00/bushel Sold $3.75/bushel Loss of $1.25/bushel |

Net Price Paid = Cash Price - futures loss or gain

Net Price Paid = $4.50 - (- $1.25 futures loss) = $5.75/bushel

Notice in this instance, the higher price is not caused by hedging but rather by inaccurately estimating the correct basis.

What if I Don't Need 5,000 Bushels of Corn?

One potential limitation to using corn futures to manage input price risk is the minimum contract size of 5,000 bushels. For many small- and medium-size livestock producers, the 5,000 bushel contract size may be larger than they need.

A useful alternative to a corn futures contract is the mini-corn futures contract. Mini contracts are offered for corn, soybeans and wheat. They afford the same protection offered by the "full-size" contracts but in 1,000-bushel contracts rather than 5,000 bushels.

The specifications and margin requirements for the various grain and oilseed contracts are presented at the end of this publication and on the CMEGroup website (http://www. cmegroup.com/market-data/delayed-quotes/commodities. html).

Hedging Summary

Hedging is a way to transfer the price risk of owning or producing a product to those who look to profit off this risk. It is a way to pre-price something you produce, store or will need to buy. When used properly it can be a very flexible pricing tool, which Georgia producers can use to control the price risk they must deal with in today's agricultural markets.

Use the following steps when making a forward-pricing decision:

- Determine the cost of production for the product. This is the only way to determine whether pricing opportunities are profitable.

- Localize the futures price by determining your local basis for the time, place, quality and quantity you will be selling. Compare these prices to cash contract prices available at the same time.

- Determine the risk of producing an un-priced commodity. For instance, how high or low do you think prices could be when you actually sell the product? Can you afford the price risk that might actually be at the lower extreme?

- Develop a pricing plan based on your operations and stick to it. Changing plans in midstream usually results in eventual dissatisfaction with forward pricing.

If you do decide to manage price risk through the futures market, remember these precautions:

- Margin money must be available if you are to hold a hedge.

- Don't let your broker make pricing decisions for you. Use his or her information and advice but remember that only you can decide what is best for your operation.

- Don't combine hedging and speculating. If you want to speculate in futures, keep separate accounts. No one ever lost a farm through true hedging; many have through speculation.

- Don't hedge until you know what you are doing. "Paper trade" until you are certain you understand the hedging process.

- Don't hedge until you investigate and understand your local basis.

For a more detailed discussion of basis and actual basis estimates for grains and livestock in Georgia, contact your county Extension agent for "Basis Tables For Georgia Feeder Cattle, Hogs, Corn and Soybeans, " Extension Marketing Department, Special Report 169.

Table 1. Futures Contract Specifications for Various Commodities

| Item | Corn | Soybean | Soybean Meal | Live Cattle | Feeder Cattle |

| Contract Size | 5,000 bushels | 5,000 bushels | 100 short tons | 40,000 pounds | 50,000 pounds |

| Deliverable Grade/Product Description | #2 Yellow at contract price, #1 Yellow at a 1.5 cent/bu premium, #3 Yellow at a 1.5 cent/bu discount | #2 Yellow at contract price, #1 Yellow at a 6 cent/bu premium, #3 Yellow at a 6 cent/bu discount | 48% Protein Soybean Meal | 55% Choice, 45% Select, Yield Grade 3 live steers | 650-849 pound steers, medium-large #1, and medium-large #1-2 |

| Contract Months | Mar, May, Jul, Sep, Dec | Jan, Mar, May, Jul, Aug, Sep, Nov | Jan, Mar, May, Jul, Aug, Sep, Oct, Dec | Feb, Apr, Jun, Aug, Oct, Dec | Jan, Mar, Apr, May, Aug, Sep, Oct, Nov |

| Last Trade Date | The business day prior to the 15th calendar day of the contract month. | The business day prior to the 15th calendar day of the contract month. | The business day prior to the 15th calendar day of the contract month. | Last business day of the contract month. | Last Thursday of the contract month with exceptions for November and other months. |

Table 2. Number of cattle required to make 50,000 pounds at various animal weights

| Sales weight (lbs.) | Number of head covered by one futures contract |

| 500 | 100 |

| 550 | 91 |

| 600 | 83 |

| 650 | 77 |

| 700 | 71 |

| 750 | 67 |

| 800 | 63 |

| 850 | 59 |

Status and Revision History

Published on Jun 17, 2014