Annual Publication

130-2-15

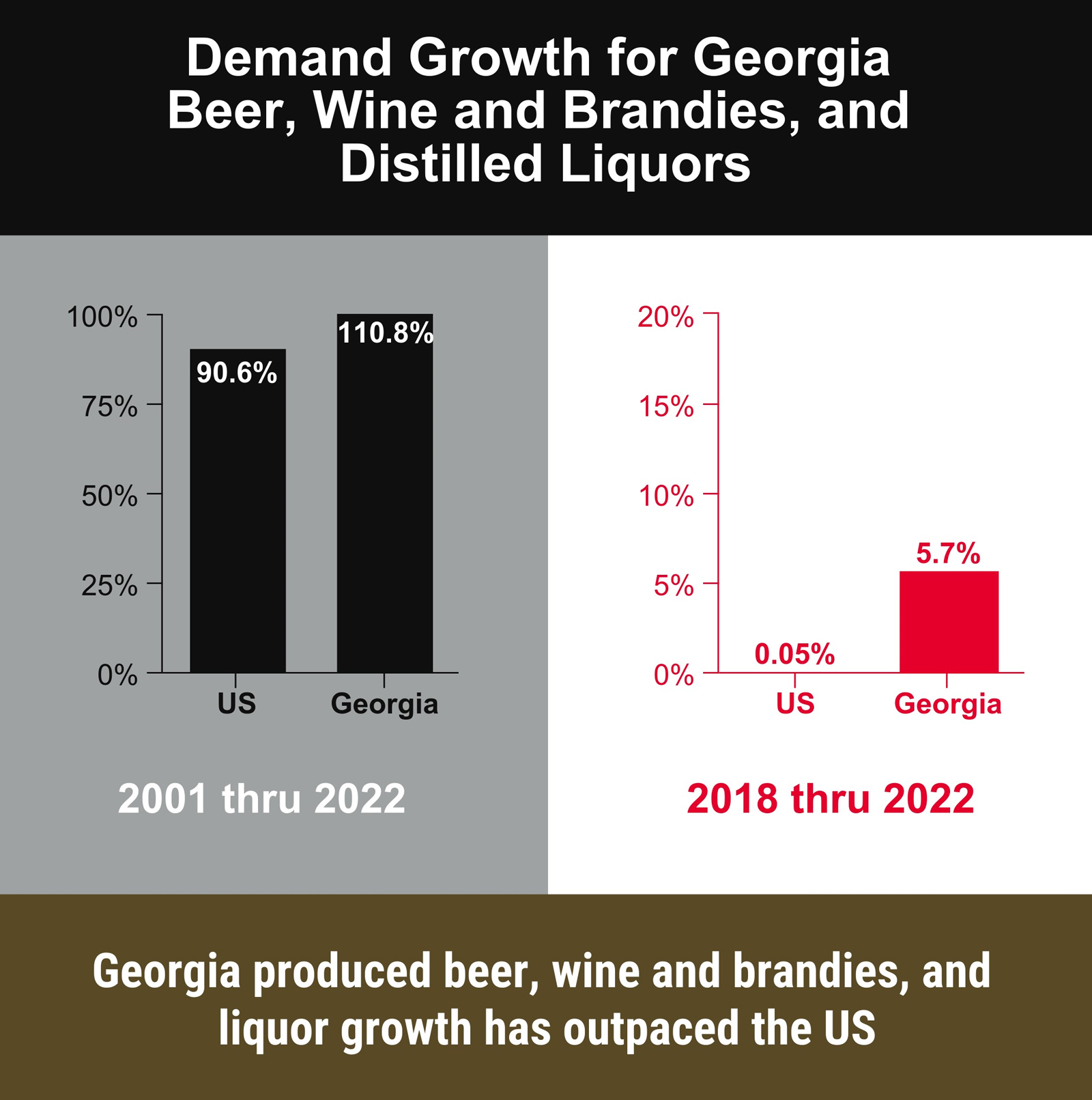

Main Takeaways

- All three alcoholic beverage sectors in Georgia—breweries, wineries, and distilleries—experienced significant growth over the last 20 years and are poised to keep growing.

- Breweries had the highest total demand in 2022 ($1.1 billion), followed closely by wineries ($970 million). Distilleries saw the highest 5-year growth rate—averaging 6% year over year.

- The trend in sourcing local ingredients will continue to help beverage producers in the state differentiate themselves from competitors and meet increased consumer demand.

- Agritourism demand and the ability to sell directly to the consumer will keep playing a critical role in the growth and development of Georgia’s beverage industry.

Industry Trends and Outlook

While consumer demand for alcoholic beverages, especially craft and premium products, has continued to increase (see Market Overview for details), an important contributor to this growth is beverage producers being able to open their businesses to the public. Most establishments in Georgia are open for visitation, which typically includes tours, tastings, and opportunities to purchase products directly. This component is critical, as many producers do not have distribution contracts where their products can be sold at retail to the consumer. This sector comprises the second-highest agritourism category within the Georgia Department of Agriculture’s agritourism database, and it continues to bolster the industry’s expansion within the state.

Given the highly competitive national and Georgia markets, beverage producers must find ways to differentiate themselves. Producers can benefit from a trend that’s now standard in the restaurant and food industry: the farm-to-table movement. Breweries, wineries, and distilleries all can source at least some local ingredients, from primary inputs to flavoring agents.

Because hops do not grow well in Georgia’s climate—limiting brewers’ ability to source one of beer’s primary ingredients locally—brewers focus on other ingredients found throughout the state. In addition to fruits used for flavoring, such as satsuma mandarins and various berries, other ingredients that are produced in Georgia, such as chocolate or honey, are being added to beers to create unique final products.

For winemakers, the primary local ingredient is grapes, as well as other fruit juices that, once fermented, produce palatable wine (e.g., blueberries or blackberries). Georgia has long featured wine made from its native grape, the muscadine (Vitis rotundifolia). Though there is an established tradition of producing variations of muscadine wine throughout the state, production volume has remained low. For the last several decades, American’s preference has been for drier European-style wines made from Mediterranean grape varietals not suited to Georgia’s climate. In efforts to capture a sizeable market demand for wines less sweet than muscadine or fruit wines, winemakers in the state have been experimenting with different native and hybrid grape varietals that produce drier wines, as well as developing new flavor profiles of muscadine wine, like refined dessert wines to European-style, dry white table wine.

Distilleries in Georgia are also looking more local, but because certain spirits need to be made from specific ingredients to create their recognizable profile, there are limitations to what can be sourced locally. For example, blue agave—the primary ingredient for making tequila— is only grown for mass production in Mexico; likewise, rum distillers must import their main ingredient, sugar cane/molasses. Georgia does, however, claim the only rum distillery in the United States that sources their own, estate-grown sugar cane for production. To work around the challenges in sourcing key ingredients locally (in-state or domestically) and meet consumer demand for more localized products, distillers are using other unique methods or ingredients to differentiate themselves. This can happen in the production process, such as adding locally grown ingredients like herbs and botanicals, or the aging process, such as using local barrels. Though it is less expensive to source other primary inputs such as corn, rye, or wheat from outside the state, there are distilleries throughout Georgia that are starting to source these ingredients locally and can leverage the higher costs through the added value of producing and marketing a local product.

Market Overview

Georgia’s alcoholic beverage industry is comprised of three types of establishments: breweries—primarily engaged in brewing beer, ale, lager, malt liquors, and nonalcoholic beer; wineries—primarily engaged in one or more of the following: (a) growing grapes and manufacturing wines and brandies; (b) manufacturing wines and brandies from grapes and other fruits grown elsewhere; and (c) blending wines and brandies; and distilleries—primarily engaged in one or more of the following: (a) distilling potable liquors except brandies; (b) distilling and blending liquors; and (c) blending and mixing liquors and other ingredients.

Consumption of alcoholic beverages in the U.S. has remained relatively steady over the last 30 years, averaging around 2.2 gallons of ethanol per capita until around 2008, when it began to increase to 2.5 gallons in 2021. As for Georgia, it ranks fourth to last in the country in terms of consumption, averaging just 1.9 gallons per capita. Looking at national trends, overall sales (wholesaler and retailer) and value of inventories have increased steadily since 2001. According to the Bureau of Labor Statistics, there was a drastic increase in the United States from about 1500 breweries, wineries, and distilleries in 2001 to more than 11,300 in 2021. Breweries held the largest market share in terms of number of establishments, just slightly ahead of wineries.

Data from IMPLAN analysis reflects a similar growth pattern in terms of economic contribution. Gross final demand (GFD)—the sum of the value of goods and services sold to final users (a similar metric to GDP)—for these beverage sectors in the United States reached an all-time high at $80.79 billion in 2022, doubling since 2001. Georgia’s GFD for these sectors follows a similar pattern—increasing from $1.23 billion in 2001 to $2.60 billion in 2022, with nearly $400 million in growth occurring in the last 5 years. Georgia ranks 9th in contribution to the U.S. GFD with more than 3% of the total, almost double the average contribution per state.

Breweries

Breweries are the largest sector of the beverage industry, and in 2021, the United States was the second-largest country in worldwide beer production behind China. According to the BLS, the number of U.S. breweries remained relatively level until 2010, grew incrementally until 2013, and then rapidly increased from 1,600 breweries to more than 5,000 by the end of 2020. Georgia’s brewery industry also grew similarly, reflecting a national trend of independent craft breweries entering the marketplace and exploding in popularity. According to the Brewers Association, which represents independent and craft breweries in the United States, Georgia ranked 18th in the country with about 170 affiliated breweries, more than three times as many as there were registered in 2016.

Georgia’s breweries were the largest contributor economically of all three sectors in the alcoholic beverage category. IMPLAN data showed the GFD for breweries in 2022 was nearly $1.1 billion, the highest it’s been in the last 5 years but down from the peak years of 2014–2018 ($1.28 billion and $1.22 billion in 2015 and 2017, respectively). This may suggest that even though the wave of craft breweries entering the market has subsided, there is an upward growth trajectory for the industry moving into 2024.

Wineries

The U.S. winery sector has increased substantially over the last 20 years, from a little over 1,000 wineries in 2001 to more than 5,000 in 2020, making wineries the second largest share of beverage manufacturing establishments in the country. The industry is dominated by California, which has around 2,000 wineries. Georgia currently ranks 17th in the country with 48 wineries. There were only a handful of wineries in the state until 2008 when a significant spike in development began. This accelerated growth period lasted until 2018 when the number of new establishments slowed.

The economic impact of Georgia wineries has also mirrored national and state trends, with an increase in GFD from $270 million in 2001 to roughly $970 million in 2022. After peaking in 2018 and declining in the wake of the pandemic, final demand rebounded sharply for 2021 and continues to grow.

Distilleries

The distillery sector of the beverage industry has also experienced significant gain, nationally and in Georgia, over the last 20 years. According to the BLS, the number of distilleries in the U.S. has increased by more than 2,000%, from 66 establishments in 2001 to 1,424 in 2021, with a sharp surge beginning around 2014 and the biggest increase between 2017 and 2021. As of 2021, Georgia had 33 active distilleries and ranked 14th nationally in number of establishments.

Similarly the GFD for Georgia distilleries has expanded considerably; from 2001 to 2022, GFD increased from $167 million to $574 million. Aside from a dip in demand for the 2 years after 2008, and a slight drop (-1%) in 2017, Georgia distilleries have experienced year-over-year gains with the last 5 years’ GFD increasing 9%, 1.3%, 9.4%, 6%, and 8%, respectively.

Status and Revision History

In Review on Jan 19, 2024

Published on Jan 22, 2024